Business model analysis: an essential management tool

The last few years have seen a growing interest in analyzing the business models of financial institutions from all angles: regulators and supervisors show concern about the viability and sustainability of financial institutions, financial institutions review their own business models, and the academic world is giving more and more attention to this matter. While this was already a matter of concern in all these areas (see Llewellyn (1999)), it was the various collapses caused by the financial crisis that spurred interest in this topic.

This is currently in addition to the unprecedented transformation that financial institutions are experiencing in their business models: profitability is threatened by interest rates, macroeconomic uncertainty and the entry of new competitors; regulation, partly as a result of the financial crisis, makes increasingly demanding requirements in all areas of banking activity; and todays’ more sophisticated technology and savvier customers are putting a big question mark on banks’ traditional way of doing business.

Business Model Analysis

In more detail, some of the main factors defining the environment in which financial institutions have been operating in recent years are:

- A macroeconomic environment in which higher growth coexists with some risks and uncertainties, which in the main developed economies is reflected in sustained but moderate GDP growth levels, private sector deleveraging, a prolonged period of low inflation and interest rates at historical lows, and an improvement in unemployment that partly helps to contain default levels. Added to this is the changing growth pattern of some of the world's major economies (e.g. China, Russia and Brazil).

- A regulatory environment that is increasingly demanding and complex in all areas: (i) capital and provisions (Basel III; changes to the regulatory capital calculation methods for key risks, requirements on the balance sheet structure (TLAC, MREL); capital planning, ICAAP and ILAAP, stress testing, IAS 39 and IFRS 9 in loan provisions); (ii) information and reporting (BCBS239, FINREP, COREP, STE, AnaCredit, AQR, Asset Encumbrance, EMIR, FATCA, New ECB Data Framework, etc.); and (iii) other requirements (conduct, compliance, model risk management, ring fencing, corporate governance and resolution plans, etc.). This coincides in time with a supervisory process in the area of transformation, marked in Europe by the creation of the Single Supervisory Mechanism (SSM) and the Supervisory Review and Evaluation Process (SREP), which harmonizes and raises the bar in banking supervision.

- An unprecedented technological transformation, characterized by an exponential increase in the ability to generate, access, store, process and model information. This in turn leads to changes in customer behavior, particularly in the use of digital channels and social networks, and to the emergence of new non-bank competitors, including a significant number of non-regulated financial intermediaries (shadow banks) and technology-intense companies with new business models (fintechs).

All this puts increasing pressure on profitability, mainly as a result of lower interest rates. According to the Fed, banks' financial margins have declined by more than 100 bps since 2000, 70 of them in the last 5 years, both for assets (narrower margin on loans, but also on securities and other assets) and for liabilities (regulatory requirements on the financing structure and reluctance to applying negative rates to deposits, making it difficult to take advantage of the low interest rate environment).

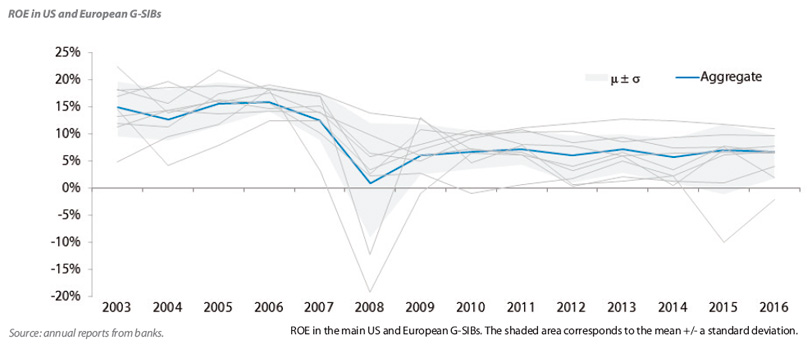

To some extent, this landscape has come about as a result of the financial crisis that started in 2007, which has significantly reduced bank profitability: ROE levels, which were often above 15% before the crisis, are now close to the cost of capital (often even below it) in the economies with the highest banking penetration levels.

As a result, there is explicit concern on the part of entities, regulators and supervisors about the insufficiency of these ROE levels to meet costs. In the words of Danièle Nouy: “The return on equity realised by banks in the euro area is still well below their costs of equity”.

This concern about profitability does not have an obvious solution: banks try a combination of cost reduction, both in the more traditional approach (branches, sizing) and in a more disruptive one (digitization), with revenue increases (pricing, fees and commissions).

In this context, business model analysis (BMA) is all the more relevant and, within it, so is business risk or strategic risk management, defined as: “The current or prospective risk to earnings and capital arising from changes in the business environment and from adverse business decisions, improper implementation of decisions or lack of responsiveness to changes in the business environment”.

Business risk, thus understood, is receiving considerable attention from regulators and supervisors:

- The ECB places it as a top supervision priority, and in SREP it effectively devotes one of its four blocks of analysis to assessing the business model, on the same level as the assessment of risk governance and risk, capital and liquidity management.

- For the first time, the EBA publishes a guide that explains how it should be monitored, and introduces business model analysis (BMA) as a supervisory tool to determine business model viability (for the following 12 months), sustainability (for the following 3 years) and key business model vulnerabilities for each supervised financial institution.

- The Fed uses the business model as a fundamental basis for determining the depth and type of supervision14 and, for the CCAR exercise, requires detailed projections of income and expenses as well as an explanation of expected changes in the financial institution’s business model.

Moreover, there is increasing concern about the potentially systemic nature of business risk, since: “Low profitability is obviously a major concern for the stockholders of banks. And it is also a concern for supervisors. Over the long term, low profitability threatens the ability of banks to generate capital and access financial markets. Ultimately, a lack of profitability affects the stability of banks.”

Against this backdrop, this paper aims to provide a detailed and comprehensive view of the supervisors’ analysis of the business model. The document is structured in three sections with three objectives:

- Describe the new banking business environment by analyzing the macroeconomic, regulatory and technological context, describing the key components underlying banks’ changing profitability.

- Explain the Business Model Analysis (BMA) concept as well as different supervisory approaches to it, with a special emphasis on the European Union.

- Summarize the industry’s response to the BMA supervisor, focusing on the different tools and metrics used by banks for business model analysis purposes.

For more information, click here to access the full document in pdf (also available in Spanish and Portuguêse).